In this edition of Value of Vanadium: Insights from VR8 we will review the market outlook and key drivers behind the growth in demand for vanadium. In addition, we are also pleased to announce the details of a memorandum of understanding (MOU) between VR8 and China Energy International Group (CEIG).

Overview

The global vanadium market size was US$ 38.97bn in 2022 and is expected to reach US$ 61.79bn by 2032, equating to a compound annual growth rate (CAGR) of 4.7% over this period.

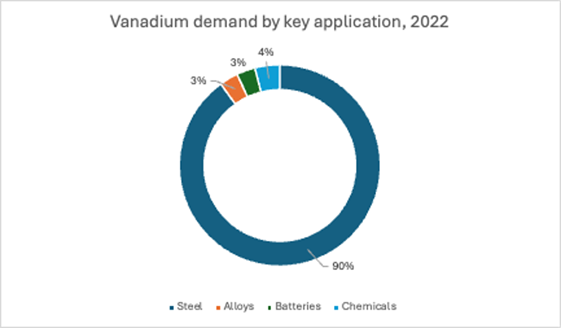

Steel dominates vanadium consumption, accounting for >90% of vanadium demand, while alloys and chemicals markets represent mature, first-use sectors for vanadium consumption. Batteries, used for energy storage applications, account for a small percentage of vanadium demand, but recent global interest has meant vanadium flow batteries are estimated to experience a substantial CAGR of 15.8% from 2024 to 2030.

In July 2024, China announced a revision of its national rebar standards, which is set to go into effect in September 2024. This is expected to increase demand for vanadium nitrogen and silicomanganese amid a push for developing high-quality steel.

Source: Project Blue

China’s Impact on the Vanadium Market

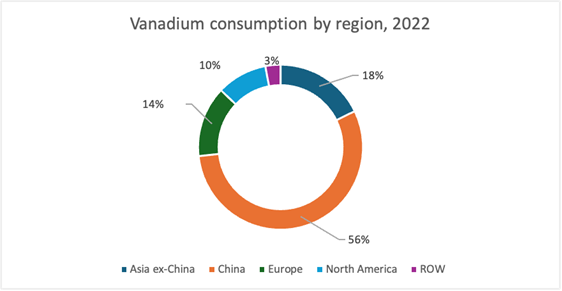

China accounts for more than half of global vanadium consumption. This is on account of the country’s recent rise in construction activity, its substantial steel sector, and the recent trend toward the production of higher quality micro-alloyed steels. These macro and micro trends and economic shifts in China have had a direct impact on the vanadium market.

Source: Project Blue

Market Driver: Steel

Vanadium demand trends are mostly driven by its use in steel, especially high-strength low-alloy (HSLA) steel. Vanadium increases the tempering stability of quenched steel and produces a secondary hardening effect.

Increased vanadium demand in steel applications is not just a factor of higher steel output (although crude steel production, driven by the demand from China, has increased substantially in the past decade). It is also because the intensity of vanadium usage in steel has increased over time. This means that more grams of vanadium are now being consumed per ton of crude steel produced.

This intensity trend originated from new construction standards in China mandating the use of micro-alloyed steel in reinforcing bars (also referred to as rebar).

Steel Market Outlook

According to critical materials market researcher, Project Blue, steel production in China reached its peak in 2020 at a level of 1,065 million tons (Mt). Over the past two decades, driven by urbanisation and industrialisation, steel production in China rose at an 11% CAGR.

Entering its 14th five-year plan, China is embarking on a new chapter of its development with a focus on information technology, biotechnology, AI, aeronautics, and astronautics. It is anticipated that infrastructure projects will be more specific, targeting the development and implementation of green energies, and urban equipment optimisation, such as water treatment facilities, and high-speed railways. It is estimated that steel per unit of gross domestic product (GDP) will decline.

Meanwhile, steel production in large emerging countries is forecast to increase, underpinned by economies still in their industrialisation phase and largely exposed to construction and infrastructure.

Countries such as India, Iran, Indonesia and Vietnam, and to a slightly lesser extent,Turkey and Brazil, will drive this production. These six countries account for more than 65% of steel production growth forecasted between 2022- 2032.

Market Drivers: Rebar

Rebar is a steel bar used as a tension device in reinforced concrete and reinforced masonry structures to strengthen and aid the concrete under tension.

Concrete is strong under compression but has low tensile strength. Rebar significantly increases the tensile strength of the structure. Rebar’s surface features a continuous series of ribs, lugs or indentations to promote a better bond with the concrete and reduce the risk of slippage.

Rebar is the main source of vanadium consumption in China. China accounts for 75% of the world’s rebar production, and 85% of the vanadium consumed in steel in China is in rebar.

Rebar production in China reached 266 Mt in 2020, driven by China’s infrastructure spending in response to Covid-19. This was probably a peak for rebar production, with declines estimated in line with steel output.

Not all rebars are high strength. To address this, in July 2024, China revised its national rebar standards, which will go into effect from 25 September 2024. The new standards impose stricter requirements on production accuracy, fatigue performance, smelting methods and testing methodologies.

Although total rebar production is forecast to decline, the vanadium density is set to grow, mainly because Grade IV rebar will replace an inferior quality Grade III. This substitution will benefit vanadium consumption as Grade IV is more vanadium-dense.

The announcement of China’s new national rebar standards boosted confidence among vanadium market participants. In general, the policy is expected to be a net benefit to alloy and rebar markets.

Read more from Fastmarkets.com

Market Drivers: Energy Storage

Energy storage is essential to decarbonising the global energy system and combating greenhouse emissions.

There are a variety of energy storage systems and technologies which can be broadly grouped as either electro-mechanical (compressed/liquid air, flywheel, and pumped hydro), electro-chemical (batteries), and other (thermal, chemical, or electromagnetic). Electromechanical (mainly pumped hydro) is still the most deployed storage technology today, but batteries are catching up.

Battery Energy Storage Systems (BESS) are essential for the role they will play in renewable energy adoption. BESS devices store energy from renewable sources such as wind and solar and allow energy to be released when required. Currently, lithium-ion batteries are the most popular BESS technology, however, the vanadium flow battery is increasingly rising in popularity as a future solution. Read our earlier newsletter comparing vanadium flow batteries to lithium-ion batteries here.

The outlook for BESS is positive. The 2022, Guidehouse Insights study forecasts annual installed vanadium flow battery utility scale and commercial and industrial battery deployment energy capacity to reach over 30 GWh by 2032. Project Blue’s outlook is more conservative at 5 GWh in 2030, but also anticipates substantial growth in the installed capacity of vanadium flow batteries, which is estimated to deliver 22,000t of vanadium in 2032 alone.

In China, the rapid deployment of large, grid-scale battery flow technology systems has also been noted by Vanitec, which is increasingly being integrated with other BESS technologies such as lithium-ion batteries.

Vanadium Demand Outlook

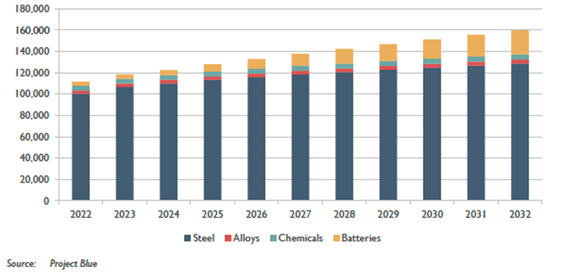

As countries focus on industrialisation and bolstering their technological advancements, the demand for vanadium is also anticipated to rise.

The market is expected to see a growth of 3.7% per year over the coming decade. A sizable portion is attributed to vanadium flow battery growth, with steel, alloy and chemical demand set to see more modest consumption gains.

Outlook for vanadium by key application (kt V)

South Africa’s Role in Preparing for the Future

South Africa is the 3rd largest producer of vanadium overall but is the largest primary producer of vanadium. In other words, South Africa produces vanadium as a primary objective and not as a result of the production of steel.

South Africa’s Bushveld Complex is one of the largest and highest-grade vanadium endowments on earth. The local industry has the opportunity to play a major role in the global transition from fossil fuel to renewable energy generation and storage, through the production of vanadium for use in the manufacture of vanadium flow batteries. This will also greatly assist with the development of a home-grown renewable energy generation and storage industry which could become an increasingly important part of SA’s base load power generation and may ultimately improve power reliability within the country.

VR8 will be a part of South Africa’s success

VR8 is striving to become a world-class producer of vanadium pentoxide and is on track to achieve this ambition. VR8’s operations are strategically located in SA’s Bushveld Region and are surrounded by approximately thirty-five mining & smelting operations, giving us access to infrastructure, contractors, engineers and a wealth of expertise.

MOU between China Energy International Group and VR8

VR8 is delighted to enter into an exclusive MOU with CEIG, a global market leader in the field of engineering, construction and renewable energy.

The purpose of the MOU is to commence negotiations for the supply of Engineering, Procurement and Construction (EPC) services and assistance for financing for Steelpoortdrift, including solar and vanadium flow battery facilities and all other associated aspect of the Project.

CEIG, a global leader in EPC and renewable energy, has a strong presence in South Africa and brings a wealth of experience in delivering large-scale energy projects, including South Africa’s upcoming Mooi Plaats 283MWdc PV power plant.

The MOU is expected to strengthen the relationship between the parties, paving the way for additional value-add opportunities that could potentially transform VR8 into a vertically integrated vanadium producer.

Click here to learn more.

Steelpoortdrift Vanadium Project Update

VR8 is thrilled to announce significant progress at its world-class Steelpoortdrift Vanadium Project in South Africa. Following an extensive review of the Project’s Definitive Feasibility Study (DFS), VR8 has identified several key technical optimisations that are anticipated to accelerate cash flow and improve operational efficiencies.

These project enhancements, spearheaded by VR8’s world-class management team, reflect the Company’s commitment to establishing a globally competitive vanadium mine. With these advancements, Steelpoortdrift is poised to become a leading force in the global vanadium market, delivering sustainable, high-quality vanadium products to meet rising demand, particularly within the growing Vanadium Flow Battery market.

To read more, click here.

Conclusion

It is an exciting time for the vanadium market! The strict implementation of new rebar standards is expected to boost demand for vanadium nitrogen and silico-manganese. It is also expected to lead to the creation of a premium for high-quality rebar products.

According to a calculation based on China’s 2023 rebar production volume, the production of rebar with the new standard will increase per annum vanadium nitrogen consumption by roughly 15%. VR8 is well positioned to cater to future demands!

Thank you for taking the time to read our latest newsletter. To read previous editions, please click on the following links:

References:

Project Blue, Fastmarkets.com